Capitalism, The Fed and Economic Policy

Comments

-

Halifax2TheMax said:Lerxst1992 said:Halifax2TheMax said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

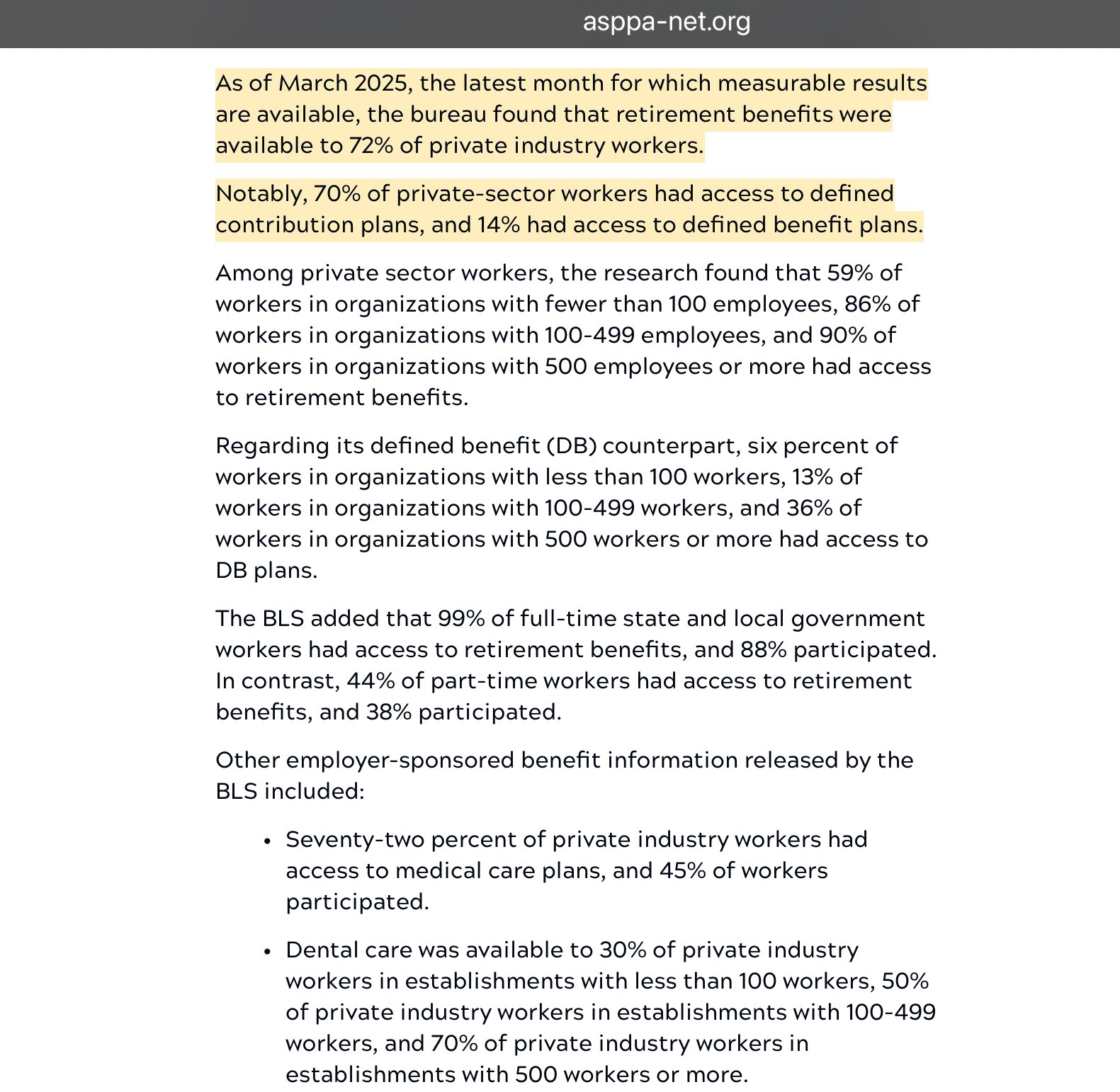

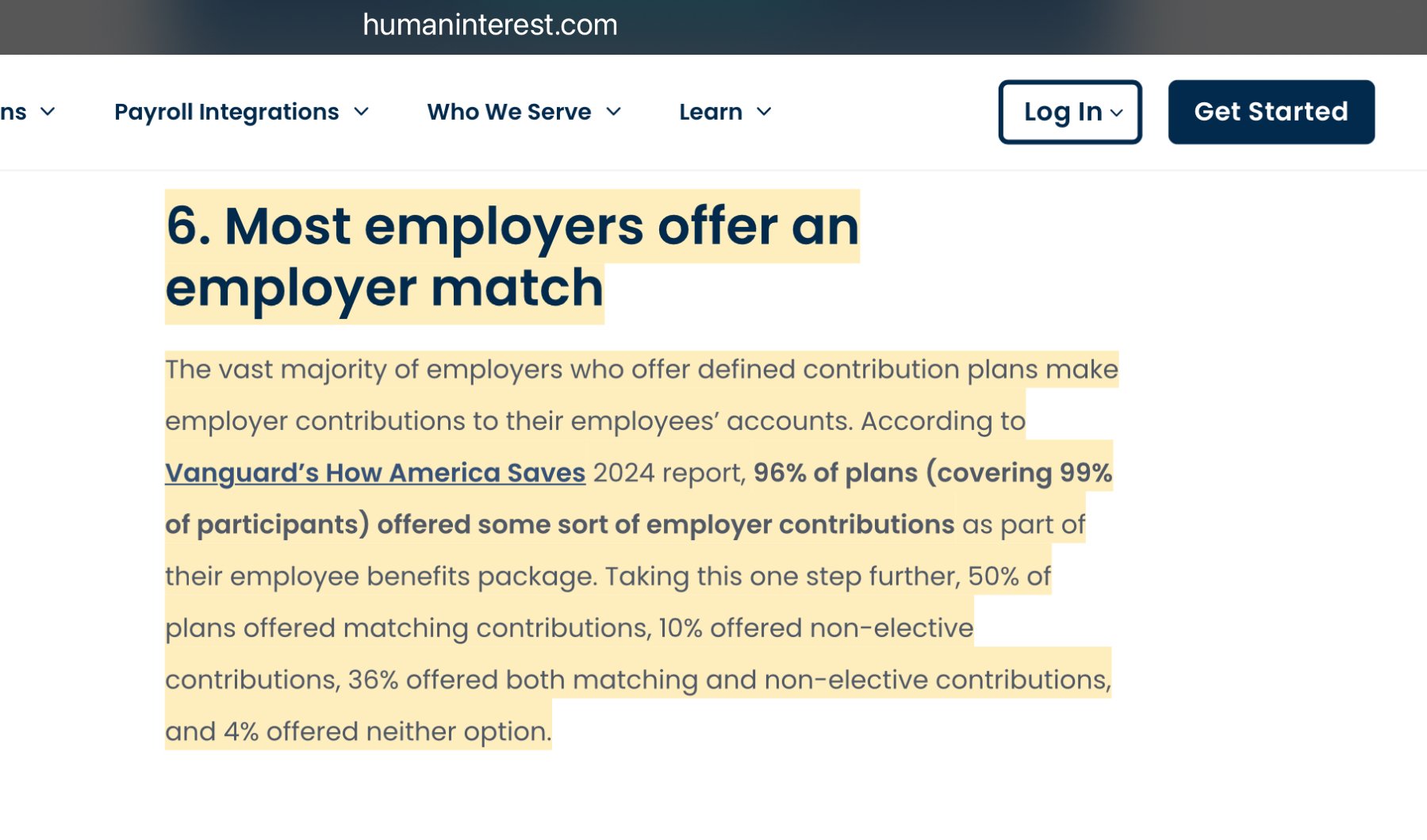

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Regardless, it’s dismissive of who and under what conditions those 33-42% of full time workers who don’t have a plan to access, and if they do, the employer doesn’t contribute. Even Wally Mart while extolling the virtues of how they’re such a great place to work doesn’t list retirement benefits as a perk, probably because you have to be full time, for a certain period of time and become “vested.”

Why no link, just screen shots?

Sorry, but I’ve got to “disappear” because I’m working on booking my 12-16 summer shows across 10 European cities with the new drummer.

The link is in part of the screen shot and there is enough info there to find the site if you think I’m some sort of adobe creative type that is drawing fake websites. At least I’m backing up my data.

And there is no way to use your stats to make the conclusion you are trying to make. The data says most employers provide retirement plans, and the small companies that don’t offer it , you think that supports whatever it is you think you are claiming?…how many of those are self employed individuals with small businesses? Are you even aware how phenomenal the self employed retirement tax benefits are? They would absolutely fall into your phantom category of no 401k.No country generates new millionaires like the USA, and there are tools for middle class workers to save and invest to help them along. But sure, let’s convert the country to mamdani socialism. Ironically, a lot of those young millionaires love him in Bushwick and Bed stuy. And it all starts with 23 year olds cutting back on their Starbucks a few times a week, if they don’t have the money elsewhere to save and invest.* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

To the bold, are you claiming that every full time employed ‘Murikkkan has an employer provided retirement plan with or without contributions? What’s in your pipe, bro?

Your inability to comprehend is astounding. AI much? I never said the number of FT working ‘Murikkkans with access to an employer sponsored retirement plan was zero. Simply pointing out that not every working ‘Murikkkan does have access nor does every employer provide a contribution. Further, the number of FT, year round workers that earn $35K or less, numbering 30-35M probably can’t afford the 5% to save for a house, given the cost of living in general, and even if they can and do, it’s hardly amounting to a down payment for a house as you advocate, even with generous raises and stock market performance. Is someone earning $35K middle class to you? WTF? It’s like your argument using averages. Bunk.

Someone who can afford an $80,000 per month apartment in Brooklyn can afford a 2% tax increase to support subsidized, free public buses. If not, or more likely they won’t, they can move to Flo Rida or Tejas. Hope they enjoy the pizza and vibrancy.

Why don’t you post the links? Tip: it’s easier than posting a screenshot and provides more information in context. But you do you.

And talk about mixing up topics, no one is saying The Bus Driver policies are dem party policies or applicable across the country. We’re discussing The Bus Driver’s policies and their impact on NYC. Which will be, if passed and implemented, “taxation with represent”. Sheesh. But now, if you’re in your twenties, give up 2-3 Starbucks a week, put that money in the stock market and you too can be a MILLIONAIRE! Good lord. Easy-peasy.

I need to “disappear” now because when I wake up, it’ll be 1975.

Your commment, without support, was

“ 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan ”

Of course you are including self employed employers in your stats, but Where’s your support? You attack image support but you provide nothing. I did, but of course facts are never good enough for you. Back to some hypothetical anecdotal example that proves your vision of the world. Every metric says that closer to 90% have access to a type of retirement vehicle to get access to beneficial tax tools.

is your entire point your $35k example? Someone earning that is given access to a residence in a high demand area like nyc? If your goal is to get those earning $35k into high rent nyc neighborhoods you are going to crash the economy. Better to give those earners tools to enhance their competitiveness in the labor market. Or housing in lower cost areas.

and you completely missed the point about the wealthy being able to afford the mamdani wealth tax. I could care less if the Koch Sisters or Bloomberg can afford this tax. They can, but the choice to pay it is up to them. Not you, not me, not Mamdani. And that was after the two week diatribe getting you to agree with the basic economic point that since wealth is concentrated at the top, it takes a small % to decide to not pay and sent the city into default, because on average, he wants to tax the elite wealth a million bucks a year to drive down their portfolios to drive down his future tax base.The micro and macro economic theory here is just plain dumb.

and no one voted for state legislators yet while ZMs plans were public, even your point on taxation with representation is completely wrong.0 -

Yay Hal, I found the site with your 42% stat on my own. Without a handout. Stay tuned for an analysis of their facts.The 42% per the site, are mostly low wage earners, and my basic point remains true, if the goal of the new socialist left is to get $35k workers into high rent neighborhoods you are going to break the economy and lose you tax base you need to cover your new socialist programs.0

-

the near term challenge for Gen Z is not about building retirement wealth, it's about having access to the full American dream that we had. That starts with home ownership and always has. That's what is out of reach for many today. They aren't thinking about their 401(s). I know this because I have two kids in their mid-20's, out of college, with good professional jobs. And they don't know how they will be able to afford a home any time soon. Today, the average age of a first time home buyer is 40!! 40!! That is nuts.Lerxst1992 said:

The bottom line is if we include all retirement tax deferral options, including defined benefit, defined contribution, SEPs, etc. the overwhelming majority of full timers have access to these wealth building tools. That’s the point where Hal was wrong. As usual, they look at one data point and believe it to be universalmrussel1 said:

According to the St Louis Fed, the total private workforce is 135MM. So 51MM (90% of 56MM) isn't that impressive.Lerxst1992 said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….…

56 million employees work for companies with greater than 100 employees. How is that not a substantial portion of the country? And if it’s not enough for you, and their employer doesn’t offer a 401k (which was Hal’s argument) they can build wealth thru other tax advantage vehicles. In that context it was a meaningless argument.

never pictured you to be the commenter on here making the anti capitalist argument.

Regardless, that's not my point nor am I anywhere near anti-capitalist. But you seem to be making an argument that affordability isn't a macro issue, it's a problem with a person's habits. And that's ridiculous. My focus is on housing and there is a clear housing crisis in this country but Trump's new prescription of 50 year mortgages will only exacerbate the issue.

The bigger point, below we blow up the free market real estate market, before the govt intervenes, there are better tax tools available right now to build wealth. That’s the point this forum and nyc voters under 45 yrs old completely ignore.

And the real estate market is NOT free market today and hasn't been since the War. Fannie and Freddie distort the free market by definition. Regardless, I'm not advocating the lending side. I think the gov't needs to figure out how to break the knot on building. Why are we not building more homes when the demand is clearly there? Look at the post-Covid boom. It wasn't a building boom, it was a buy/sale boom when homes couldn't stay on the market for more than a few hours, going for over asking. That is a distorted market right there. And then it falls apart quickly.0 -

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Keep moving those goal posts in your fear mongering. It’s not the goal to get $35K earners into high end neighborhoods, it’s to get them into affordable, quality housing. Now the Bus Driver’s going to tax that 1% a million dollars. What a joke.

The Bus Driver takes office on 1/1/26. I suppose that 1% better move by 1/2/26 if they don’t want their taxes to go up 2%, eh? Guess there’s no elections in November of ‘26, either, eh?

What are the rules regarding withdrawing money from a retirement account to use as a down payment on a house? What are the tax implications, payback requirements and further tax implications? Yea sure, none and it’s just a sure fire way to accumulate wealth and create a down payment, and it’s so easy that everyone can and should do it, particularly millennials, if they’d just give up their Starbucks and Netflix for five years. Bunk. As already pointed out, it’s not as simple as your averages or “taxation without represent” or “some access to some retirement savings (gee, social security included in that definition to up your percentage. Oh and ‘what about self-employed people and the tax benefits of being self-employed’ and what about ‘Murikkka minting more millionaires than anywhere on earth and it could be this, it could be that, I think I saw a yellow cat).

You’ve got 49 days to move before NYC falls and falls 1975 hard. BOOM!

09/15/1998 & 09/16/1998, Mansfield, MA; 08/29/00 08/30/00, Mansfield, MA; 07/02/03, 07/03/03, Mansfield, MA; 09/28/04, 09/29/04, Boston, MA; 09/22/05, Halifax, NS; 05/24/06, 05/25/06, Boston, MA; 07/22/06, 07/23/06, Gorge, WA; 06/27/2008, Hartford; 06/28/08, 06/30/08, Mansfield; 08/18/2009, O2, London, UK; 10/30/09, 10/31/09, Philadelphia, PA; 05/15/10, Hartford, CT; 05/17/10, Boston, MA; 05/20/10, 05/21/10, NY, NY; 06/22/10, Dublin, IRE; 06/23/10, Northern Ireland; 09/03/11, 09/04/11, Alpine Valley, WI; 09/11/11, 09/12/11, Toronto, Ont; 09/14/11, Ottawa, Ont; 09/15/11, Hamilton, Ont; 07/02/2012, Prague, Czech Republic; 07/04/2012 & 07/05/2012, Berlin, Germany; 07/07/2012, Stockholm, Sweden; 09/30/2012, Missoula, MT; 07/16/2013, London, Ont; 07/19/2013, Chicago, IL; 10/15/2013 & 10/16/2013, Worcester, MA; 10/21/2013 & 10/22/2013, Philadelphia, PA; 10/25/2013, Hartford, CT; 11/29/2013, Portland, OR; 11/30/2013, Spokane, WA; 12/04/2013, Vancouver, BC; 12/06/2013, Seattle, WA; 10/03/2014, St. Louis. MO; 10/22/2014, Denver, CO; 10/26/2015, New York, NY; 04/23/2016, New Orleans, LA; 04/28/2016 & 04/29/2016, Philadelphia, PA; 05/01/2016 & 05/02/2016, New York, NY; 05/08/2016, Ottawa, Ont.; 05/10/2016 & 05/12/2016, Toronto, Ont.; 08/05/2016 & 08/07/2016, Boston, MA; 08/20/2016 & 08/22/2016, Chicago, IL; 07/01/2018, Prague, Czech Republic; 07/03/2018, Krakow, Poland; 07/05/2018, Berlin, Germany; 09/02/2018 & 09/04/2018, Boston, MA; 09/08/2022, Toronto, Ont; 09/11/2022, New York, NY; 09/14/2022, Camden, NJ; 09/02/2023, St. Paul, MN; 05/04/2024 & 05/06/2024, Vancouver, BC; 05/10/2024, Portland, OR; 05/03/2025, New Orleans, LA;

Libtardaplorable©. And proud of it.

Brilliantati©0 -

mrussel1 said:

the near term challenge for Gen Z is not about building retirement wealth, it's about having access to the full American dream that we had. That starts with home ownership and always has. That's what is out of reach for many today. They aren't thinking about their 401(s). I know this because I have two kids in their mid-20's, out of college, with good professional jobs. And they don't know how they will be able to afford a home any time soon. Today, the average age of a first time home buyer is 40!! 40!! That is nuts.Lerxst1992 said:

The bottom line is if we include all retirement tax deferral options, including defined benefit, defined contribution, SEPs, etc. the overwhelming majority of full timers have access to these wealth building tools. That’s the point where Hal was wrong. As usual, they look at one data point and believe it to be universalmrussel1 said:

According to the St Louis Fed, the total private workforce is 135MM. So 51MM (90% of 56MM) isn't that impressive.Lerxst1992 said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….…

56 million employees work for companies with greater than 100 employees. How is that not a substantial portion of the country? And if it’s not enough for you, and their employer doesn’t offer a 401k (which was Hal’s argument) they can build wealth thru other tax advantage vehicles. In that context it was a meaningless argument.

never pictured you to be the commenter on here making the anti capitalist argument.

Regardless, that's not my point nor am I anywhere near anti-capitalist. But you seem to be making an argument that affordability isn't a macro issue, it's a problem with a person's habits. And that's ridiculous. My focus is on housing and there is a clear housing crisis in this country but Trump's new prescription of 50 year mortgages will only exacerbate the issue.

The bigger point, below we blow up the free market real estate market, before the govt intervenes, there are better tax tools available right now to build wealth. That’s the point this forum and nyc voters under 45 yrs old completely ignore.

And the real estate market is NOT free market today and hasn't been since the War. Fannie and Freddie distort the free market by definition. Regardless, I'm not advocating the lending side. I think the gov't needs to figure out how to break the knot on building. Why are we not building more homes when the demand is clearly there? Look at the post-Covid boom. It wasn't a building boom, it was a buy/sale boom when homes couldn't stay on the market for more than a few hours, going for over asking. That is a distorted market right there. And then it falls apart quickly.One of my earlier points was to use retirement tools today for tax savings and employer contributions to accelerate building wealth, and then use items like 401k loans for a down payment. Build wealth first, then figure out housing. Specifically the nyc plan to intervene in the real estate market is a big departure from the last 50 years. Dare I say I once knew a middle class young couple that stayed with parents first five years after college and saved $60k for a home when (edit, Vs. aka Five Against One) was dominating?

i agree it’s mostly on the building side, and the biggest problem is in blue states that are huge in nimby slow down tactics for new units. And building new units is expensive. The problem is complex. Converting low density to high is also complex. And the govt has never demonstrated the ability to take a comprehensive top down approach. Such as when the govt lowered interest rates during Covid, and now a significant number of residences will not flip on the market due to homeowners holding cheap mortgages lowering supply and raising prices.

Post edited by Lerxst1992 on0 -

You would advise your kids to borrow from their 401k? Sorry, that's terrible advice and not a real solution to the problem. And we're not just talking about low to high density. More urban condos aren't the answer. We have plenty of open real estate in this country, it's just not getting developed. Why? Maybe the cost to build is too high and therefore the margins are too low to invest. Maybe it is a permitting issue, but that's locality and this problem persists everywhere. I don't pretend to know the building cause, but I do know solutions that will not work. 50 year mortgage is number one on that list.Lerxst1992 said:mrussel1 said:

the near term challenge for Gen Z is not about building retirement wealth, it's about having access to the full American dream that we had. That starts with home ownership and always has. That's what is out of reach for many today. They aren't thinking about their 401(s). I know this because I have two kids in their mid-20's, out of college, with good professional jobs. And they don't know how they will be able to afford a home any time soon. Today, the average age of a first time home buyer is 40!! 40!! That is nuts.Lerxst1992 said:

The bottom line is if we include all retirement tax deferral options, including defined benefit, defined contribution, SEPs, etc. the overwhelming majority of full timers have access to these wealth building tools. That’s the point where Hal was wrong. As usual, they look at one data point and believe it to be universalmrussel1 said:

According to the St Louis Fed, the total private workforce is 135MM. So 51MM (90% of 56MM) isn't that impressive.Lerxst1992 said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….…

56 million employees work for companies with greater than 100 employees. How is that not a substantial portion of the country? And if it’s not enough for you, and their employer doesn’t offer a 401k (which was Hal’s argument) they can build wealth thru other tax advantage vehicles. In that context it was a meaningless argument.

never pictured you to be the commenter on here making the anti capitalist argument.

Regardless, that's not my point nor am I anywhere near anti-capitalist. But you seem to be making an argument that affordability isn't a macro issue, it's a problem with a person's habits. And that's ridiculous. My focus is on housing and there is a clear housing crisis in this country but Trump's new prescription of 50 year mortgages will only exacerbate the issue.

The bigger point, below we blow up the free market real estate market, before the govt intervenes, there are better tax tools available right now to build wealth. That’s the point this forum and nyc voters under 45 yrs old completely ignore.

And the real estate market is NOT free market today and hasn't been since the War. Fannie and Freddie distort the free market by definition. Regardless, I'm not advocating the lending side. I think the gov't needs to figure out how to break the knot on building. Why are we not building more homes when the demand is clearly there? Look at the post-Covid boom. It wasn't a building boom, it was a buy/sale boom when homes couldn't stay on the market for more than a few hours, going for over asking. That is a distorted market right there. And then it falls apart quickly.One of my earlier points was to use retirement tools today for tax savings and employer contributions to accelerate building wealth, and then use items like 401k loans for a down payment. Build wealth first, then figure out housing. Specifically the nyc plan to intervene in the real estate market is a big departure from the last 50 years. Dare I say I once knew a middle class young couple that stayed with parents first five years after college and saved $60k for a home when (edit, Vs. aka Five Against One) was dominating?

i agree it’s mostly on the building side, and the biggest problem is in blue states that are huge in nimby slow down tactics for new units. And building new units is expensive. The problem is complex. Converting low density to high is also complex. And the govt has never demonstrated the ability to take a comprehensive top down approach. Such as when the govt lowered interest rates during Covid, and now a significant number of residences will not flip on the market due to homeowners holding cheap mortgages lowering supply and raising prices.

0 -

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Whoa! I thought it was interest rates and the time-money continuum and that houses today are just as affordable as they were in 1975? Am I missing something?

09/15/1998 & 09/16/1998, Mansfield, MA; 08/29/00 08/30/00, Mansfield, MA; 07/02/03, 07/03/03, Mansfield, MA; 09/28/04, 09/29/04, Boston, MA; 09/22/05, Halifax, NS; 05/24/06, 05/25/06, Boston, MA; 07/22/06, 07/23/06, Gorge, WA; 06/27/2008, Hartford; 06/28/08, 06/30/08, Mansfield; 08/18/2009, O2, London, UK; 10/30/09, 10/31/09, Philadelphia, PA; 05/15/10, Hartford, CT; 05/17/10, Boston, MA; 05/20/10, 05/21/10, NY, NY; 06/22/10, Dublin, IRE; 06/23/10, Northern Ireland; 09/03/11, 09/04/11, Alpine Valley, WI; 09/11/11, 09/12/11, Toronto, Ont; 09/14/11, Ottawa, Ont; 09/15/11, Hamilton, Ont; 07/02/2012, Prague, Czech Republic; 07/04/2012 & 07/05/2012, Berlin, Germany; 07/07/2012, Stockholm, Sweden; 09/30/2012, Missoula, MT; 07/16/2013, London, Ont; 07/19/2013, Chicago, IL; 10/15/2013 & 10/16/2013, Worcester, MA; 10/21/2013 & 10/22/2013, Philadelphia, PA; 10/25/2013, Hartford, CT; 11/29/2013, Portland, OR; 11/30/2013, Spokane, WA; 12/04/2013, Vancouver, BC; 12/06/2013, Seattle, WA; 10/03/2014, St. Louis. MO; 10/22/2014, Denver, CO; 10/26/2015, New York, NY; 04/23/2016, New Orleans, LA; 04/28/2016 & 04/29/2016, Philadelphia, PA; 05/01/2016 & 05/02/2016, New York, NY; 05/08/2016, Ottawa, Ont.; 05/10/2016 & 05/12/2016, Toronto, Ont.; 08/05/2016 & 08/07/2016, Boston, MA; 08/20/2016 & 08/22/2016, Chicago, IL; 07/01/2018, Prague, Czech Republic; 07/03/2018, Krakow, Poland; 07/05/2018, Berlin, Germany; 09/02/2018 & 09/04/2018, Boston, MA; 09/08/2022, Toronto, Ont; 09/11/2022, New York, NY; 09/14/2022, Camden, NJ; 09/02/2023, St. Paul, MN; 05/04/2024 & 05/06/2024, Vancouver, BC; 05/10/2024, Portland, OR; 05/03/2025, New Orleans, LA;

Libtardaplorable©. And proud of it.

Brilliantati©0 -

yeah the 401k borrowing is a horrible idea...separation from service (more likely for a younger person) can require repayment in a short amount of time or result in taxable income with penalty.mrussel1 said:

You would advise your kids to borrow from their 401k? Sorry, that's terrible advice and not a real solution to the problem. And we're not just talking about low to high density. More urban condos aren't the answer. We have plenty of open real estate in this country, it's just not getting developed. Why? Maybe the cost to build is too high and therefore the margins are too low to invest. Maybe it is a permitting issue, but that's locality and this problem persists everywhere. I don't pretend to know the building cause, but I do know solutions that will not work. 50 year mortgage is number one on that list.Lerxst1992 said:mrussel1 said:

the near term challenge for Gen Z is not about building retirement wealth, it's about having access to the full American dream that we had. That starts with home ownership and always has. That's what is out of reach for many today. They aren't thinking about their 401(s). I know this because I have two kids in their mid-20's, out of college, with good professional jobs. And they don't know how they will be able to afford a home any time soon. Today, the average age of a first time home buyer is 40!! 40!! That is nuts.Lerxst1992 said:

The bottom line is if we include all retirement tax deferral options, including defined benefit, defined contribution, SEPs, etc. the overwhelming majority of full timers have access to these wealth building tools. That’s the point where Hal was wrong. As usual, they look at one data point and believe it to be universalmrussel1 said:

According to the St Louis Fed, the total private workforce is 135MM. So 51MM (90% of 56MM) isn't that impressive.Lerxst1992 said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….…

56 million employees work for companies with greater than 100 employees. How is that not a substantial portion of the country? And if it’s not enough for you, and their employer doesn’t offer a 401k (which was Hal’s argument) they can build wealth thru other tax advantage vehicles. In that context it was a meaningless argument.

never pictured you to be the commenter on here making the anti capitalist argument.

Regardless, that's not my point nor am I anywhere near anti-capitalist. But you seem to be making an argument that affordability isn't a macro issue, it's a problem with a person's habits. And that's ridiculous. My focus is on housing and there is a clear housing crisis in this country but Trump's new prescription of 50 year mortgages will only exacerbate the issue.

The bigger point, below we blow up the free market real estate market, before the govt intervenes, there are better tax tools available right now to build wealth. That’s the point this forum and nyc voters under 45 yrs old completely ignore.

And the real estate market is NOT free market today and hasn't been since the War. Fannie and Freddie distort the free market by definition. Regardless, I'm not advocating the lending side. I think the gov't needs to figure out how to break the knot on building. Why are we not building more homes when the demand is clearly there? Look at the post-Covid boom. It wasn't a building boom, it was a buy/sale boom when homes couldn't stay on the market for more than a few hours, going for over asking. That is a distorted market right there. And then it falls apart quickly.One of my earlier points was to use retirement tools today for tax savings and employer contributions to accelerate building wealth, and then use items like 401k loans for a down payment. Build wealth first, then figure out housing. Specifically the nyc plan to intervene in the real estate market is a big departure from the last 50 years. Dare I say I once knew a middle class young couple that stayed with parents first five years after college and saved $60k for a home when (edit, Vs. aka Five Against One) was dominating?

i agree it’s mostly on the building side, and the biggest problem is in blue states that are huge in nimby slow down tactics for new units. And building new units is expensive. The problem is complex. Converting low density to high is also complex. And the govt has never demonstrated the ability to take a comprehensive top down approach. Such as when the govt lowered interest rates during Covid, and now a significant number of residences will not flip on the market due to homeowners holding cheap mortgages lowering supply and raising prices.

Remember the Thomas Nine !! (10/02/2018)

The Golden Age is 2 months away. And guess what….. you’re gonna love it! (teskeinc 11.19.24)

1998: Noblesville; 2003: Noblesville; 2009: EV Nashville, Chicago, Chicago

2010: St Louis, Columbus, Noblesville; 2011: EV Chicago, East Troy, East Troy

2013: London ON, Wrigley; 2014: Cincy, St Louis, Moline (NO CODE)

2016: Lexington, Wrigley #1; 2018: Wrigley, Wrigley, Boston, Boston

2020: Oakland, Oakland: 2021: EV Ohana, Ohana, Ohana, Ohana

2022: Oakland, Oakland, Nashville, Louisville; 2023: Chicago, Chicago, Noblesville

2024: Noblesville, Wrigley, Wrigley, Ohana, Ohana; 2025: Pitt1, Pitt20 -

I thought there were anti-predatory laws passed about this?mickeyrat said:home economics should be brought back to include financial literacy.The Flex Loan, a new type of payday loan pioneered by Advance Financial in Tennessee, allows residents to borrow up to $4,000 at a 279.5% interest rate.

It has burdened low-income borrowers while generating huge profits for lenders.

Read more (published May): https://propub.li/4nUCJgX0 -

My first choice would be to yes, avoid it, but if workers under 35, invest their gross salary on 4k net pay, add in employer match, they’re investing 10k a year. Over ten years at standard return that could yield a $150k portfolio. IIRC rules correctly they can borrow at a lower rate, and the loan balance still grows if the investments grow. I agree not my first choice. Again, the comparison is to an extreme socialist policy, and this is still a better option than that.Gern Blansten said:

yeah the 401k borrowing is a horrible idea...separation from service (more likely for a younger person) can require repayment in a short amount of time or result in taxable income with penalty.mrussel1 said:

You would advise your kids to borrow from their 401k? Sorry, that's terrible advice and not a real solution to the problem. And we're not just talking about low to high density. More urban condos aren't the answer. We have plenty of open real estate in this country, it's just not getting developed. Why? Maybe the cost to build is too high and therefore the margins are too low to invest. Maybe it is a permitting issue, but that's locality and this problem persists everywhere. I don't pretend to know the building cause, but I do know solutions that will not work. 50 year mortgage is number one on that list.Lerxst1992 said:mrussel1 said:

the near term challenge for Gen Z is not about building retirement wealth, it's about having access to the full American dream that we had. That starts with home ownership and always has. That's what is out of reach for many today. They aren't thinking about their 401(s). I know this because I have two kids in their mid-20's, out of college, with good professional jobs. And they don't know how they will be able to afford a home any time soon. Today, the average age of a first time home buyer is 40!! 40!! That is nuts.Lerxst1992 said:

The bottom line is if we include all retirement tax deferral options, including defined benefit, defined contribution, SEPs, etc. the overwhelming majority of full timers have access to these wealth building tools. That’s the point where Hal was wrong. As usual, they look at one data point and believe it to be universalmrussel1 said:

According to the St Louis Fed, the total private workforce is 135MM. So 51MM (90% of 56MM) isn't that impressive.Lerxst1992 said:mrussel1 said:

Less than 3% of US companies have more than 100 employees. How is your 90% stat some winning argument?Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

“Hal” also says 42% of full time working ‘Murikkkans don’t have access to an employer sponsored retirement plan and that 50.5% that do, don’t have an employer match. Further, 22.3% of year round, full-time workers, or approximately 30-35M people, earn less than $35K.

Someone earning $35K, before taxes, who puts 5% of their annual salary into a 401K, with no employee match, a 4% annual raise and a 8% gain in their 401K, year over year, compounded, at 5 years they’d have approximately $11,835, enough for a $59K house at 20% down payment or as a first time home buyer with excellent credit and a 5% down payment, a $230,000 house. That 5% contribution is before taxes, rent, food , utilities, car payment, etc. Seeing how some posters like averages, the average cost of a house in the US is approximately $363K.

But hey, if they just give up their Starbucks and Netflix, they too can own a house in five years. Simple, easy-peasy.

back to misinformation island. I’ll post some facts, then u go hide. Mamdani island all over again…Cue up the Carly Simon band…

Misinformation

misinformation

Is making me faint….

counting all types of pension plans access for full time workers 84%; and the access for coverage is about 90% for orgs over 100 employees…and most employers match.

anticipation….…

56 million employees work for companies with greater than 100 employees. How is that not a substantial portion of the country? And if it’s not enough for you, and their employer doesn’t offer a 401k (which was Hal’s argument) they can build wealth thru other tax advantage vehicles. In that context it was a meaningless argument.

never pictured you to be the commenter on here making the anti capitalist argument.

Regardless, that's not my point nor am I anywhere near anti-capitalist. But you seem to be making an argument that affordability isn't a macro issue, it's a problem with a person's habits. And that's ridiculous. My focus is on housing and there is a clear housing crisis in this country but Trump's new prescription of 50 year mortgages will only exacerbate the issue.

The bigger point, below we blow up the free market real estate market, before the govt intervenes, there are better tax tools available right now to build wealth. That’s the point this forum and nyc voters under 45 yrs old completely ignore.

And the real estate market is NOT free market today and hasn't been since the War. Fannie and Freddie distort the free market by definition. Regardless, I'm not advocating the lending side. I think the gov't needs to figure out how to break the knot on building. Why are we not building more homes when the demand is clearly there? Look at the post-Covid boom. It wasn't a building boom, it was a buy/sale boom when homes couldn't stay on the market for more than a few hours, going for over asking. That is a distorted market right there. And then it falls apart quickly.One of my earlier points was to use retirement tools today for tax savings and employer contributions to accelerate building wealth, and then use items like 401k loans for a down payment. Build wealth first, then figure out housing. Specifically the nyc plan to intervene in the real estate market is a big departure from the last 50 years. Dare I say I once knew a middle class young couple that stayed with parents first five years after college and saved $60k for a home when (edit, Vs. aka Five Against One) was dominating?

i agree it’s mostly on the building side, and the biggest problem is in blue states that are huge in nimby slow down tactics for new units. And building new units is expensive. The problem is complex. Converting low density to high is also complex. And the govt has never demonstrated the ability to take a comprehensive top down approach. Such as when the govt lowered interest rates during Covid, and now a significant number of residences will not flip on the market due to homeowners holding cheap mortgages lowering supply and raising prices.

And to the open space non urban building solution, specifically this discussion evolved from a Mamdani approach, who wants to build at below market costs, subsidized by elite wealth, in the city.

A related note, Just announced today that … me, Tempo, and Jose are spending $800 million to subsidize an electric transmission line for the city to get renewable energy, which will “almost exclusively benefit the city.”

It’s not uncommon for the burbs to subsidize the city. I hope Nick and the others thank us personally.0 -

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

09/15/1998 & 09/16/1998, Mansfield, MA; 08/29/00 08/30/00, Mansfield, MA; 07/02/03, 07/03/03, Mansfield, MA; 09/28/04, 09/29/04, Boston, MA; 09/22/05, Halifax, NS; 05/24/06, 05/25/06, Boston, MA; 07/22/06, 07/23/06, Gorge, WA; 06/27/2008, Hartford; 06/28/08, 06/30/08, Mansfield; 08/18/2009, O2, London, UK; 10/30/09, 10/31/09, Philadelphia, PA; 05/15/10, Hartford, CT; 05/17/10, Boston, MA; 05/20/10, 05/21/10, NY, NY; 06/22/10, Dublin, IRE; 06/23/10, Northern Ireland; 09/03/11, 09/04/11, Alpine Valley, WI; 09/11/11, 09/12/11, Toronto, Ont; 09/14/11, Ottawa, Ont; 09/15/11, Hamilton, Ont; 07/02/2012, Prague, Czech Republic; 07/04/2012 & 07/05/2012, Berlin, Germany; 07/07/2012, Stockholm, Sweden; 09/30/2012, Missoula, MT; 07/16/2013, London, Ont; 07/19/2013, Chicago, IL; 10/15/2013 & 10/16/2013, Worcester, MA; 10/21/2013 & 10/22/2013, Philadelphia, PA; 10/25/2013, Hartford, CT; 11/29/2013, Portland, OR; 11/30/2013, Spokane, WA; 12/04/2013, Vancouver, BC; 12/06/2013, Seattle, WA; 10/03/2014, St. Louis. MO; 10/22/2014, Denver, CO; 10/26/2015, New York, NY; 04/23/2016, New Orleans, LA; 04/28/2016 & 04/29/2016, Philadelphia, PA; 05/01/2016 & 05/02/2016, New York, NY; 05/08/2016, Ottawa, Ont.; 05/10/2016 & 05/12/2016, Toronto, Ont.; 08/05/2016 & 08/07/2016, Boston, MA; 08/20/2016 & 08/22/2016, Chicago, IL; 07/01/2018, Prague, Czech Republic; 07/03/2018, Krakow, Poland; 07/05/2018, Berlin, Germany; 09/02/2018 & 09/04/2018, Boston, MA; 09/08/2022, Toronto, Ont; 09/11/2022, New York, NY; 09/14/2022, Camden, NJ; 09/02/2023, St. Paul, MN; 05/04/2024 & 05/06/2024, Vancouver, BC; 05/10/2024, Portland, OR; 05/03/2025, New Orleans, LA;

Libtardaplorable©. And proud of it.

Brilliantati©0 -

Halifax2TheMax said:

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.0 -

In Tennessee, they passed a law that allows "fees" to be charged daily, just like interest. But it's reclassified.tempo_n_groove said:

I thought there were anti-predatory laws passed about this?mickeyrat said:home economics should be brought back to include financial literacy.The Flex Loan, a new type of payday loan pioneered by Advance Financial in Tennessee, allows residents to borrow up to $4,000 at a 279.5% interest rate.

It has burdened low-income borrowers while generating huge profits for lenders.

Read more (published May): https://propub.li/4nUCJgX0 -

You seem to keep focusing on NYC, but that's not the problem for most of us, so I'm not engaging in conversation about your new mayor's priority. But acting like the problems of affordability is really on the individual decisions on netflix or whatever is pretty tone deaf and the exact tact of Trump. It's going to bury them in the midterms if your/his perspective remains the same.Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.0 -

Lerxst1992 said:Halifax2TheMax said:

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

I don’t give any of my money to Jeff Bozos via any of his channels. Don’t shop at whole foods, don’t shop/buy on Amazon and I don’t stream/watch anything on prime. Fuck him.

09/15/1998 & 09/16/1998, Mansfield, MA; 08/29/00 08/30/00, Mansfield, MA; 07/02/03, 07/03/03, Mansfield, MA; 09/28/04, 09/29/04, Boston, MA; 09/22/05, Halifax, NS; 05/24/06, 05/25/06, Boston, MA; 07/22/06, 07/23/06, Gorge, WA; 06/27/2008, Hartford; 06/28/08, 06/30/08, Mansfield; 08/18/2009, O2, London, UK; 10/30/09, 10/31/09, Philadelphia, PA; 05/15/10, Hartford, CT; 05/17/10, Boston, MA; 05/20/10, 05/21/10, NY, NY; 06/22/10, Dublin, IRE; 06/23/10, Northern Ireland; 09/03/11, 09/04/11, Alpine Valley, WI; 09/11/11, 09/12/11, Toronto, Ont; 09/14/11, Ottawa, Ont; 09/15/11, Hamilton, Ont; 07/02/2012, Prague, Czech Republic; 07/04/2012 & 07/05/2012, Berlin, Germany; 07/07/2012, Stockholm, Sweden; 09/30/2012, Missoula, MT; 07/16/2013, London, Ont; 07/19/2013, Chicago, IL; 10/15/2013 & 10/16/2013, Worcester, MA; 10/21/2013 & 10/22/2013, Philadelphia, PA; 10/25/2013, Hartford, CT; 11/29/2013, Portland, OR; 11/30/2013, Spokane, WA; 12/04/2013, Vancouver, BC; 12/06/2013, Seattle, WA; 10/03/2014, St. Louis. MO; 10/22/2014, Denver, CO; 10/26/2015, New York, NY; 04/23/2016, New Orleans, LA; 04/28/2016 & 04/29/2016, Philadelphia, PA; 05/01/2016 & 05/02/2016, New York, NY; 05/08/2016, Ottawa, Ont.; 05/10/2016 & 05/12/2016, Toronto, Ont.; 08/05/2016 & 08/07/2016, Boston, MA; 08/20/2016 & 08/22/2016, Chicago, IL; 07/01/2018, Prague, Czech Republic; 07/03/2018, Krakow, Poland; 07/05/2018, Berlin, Germany; 09/02/2018 & 09/04/2018, Boston, MA; 09/08/2022, Toronto, Ont; 09/11/2022, New York, NY; 09/14/2022, Camden, NJ; 09/02/2023, St. Paul, MN; 05/04/2024 & 05/06/2024, Vancouver, BC; 05/10/2024, Portland, OR; 05/03/2025, New Orleans, LA;

Libtardaplorable©. And proud of it.

Brilliantati©0 -

He only owns 8% of Amazon. I give them money. But then again, I made a hefty investment in 2008 into Amzn, so I'm a fan.Halifax2TheMax said:Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

I don’t give any of my money to Jeff Bozos via any of his channels. Don’t shop at whole foods, don’t shop/buy on Amazon and I don’t stream/watch anything on prime. Fuck him.

0 -

Halifax2TheMax said:Lerxst1992 said:Halifax2TheMax said:

* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

I don’t give any of my money to Jeff Bozos via any of his channels. Don’t shop at whole foods, don’t shop/buy on Amazon and I don’t stream/watch anything on prime. Fuck him.

Guess gonna “prime for the game tonight” was an excellent deepfake.0 -

mrussel1 said:

You seem to keep focusing on NYC, but that's not the problem for most of us, so I'm not engaging in conversation about your new mayor's priority. But acting like the problems of affordability is really on the individual decisions on netflix or whatever is pretty tone deaf and the exact tact of Trump. It's going to bury them in the midterms if your/his perspective remains the same.Lerxst1992 said:Halifax2TheMax said:* The following opinion is mine and mine alone and does not represent the views of my family, friends, government and/or my past, present or future employer. US Department of State: 1-888-407-4747.

Somebody ought to tell those 32.8M households that if they just forgo their daily Starbucks and Netflix subscription and put that savings into the stock market, they too can be millionaires. Maybe even buy a house someday. You could also put the advice in a nice slick, glossy, printed package and sell it to them for a hundred or two hundred a pop and if they buy now, attend your amazing seminar for half off and the low, low price of $650. Hey, but fuck these people with their under employment, lack of affordable healthcare, going out of business family business and stagnant wages. And if they have kids? A double fuck you. But maybe, just maybe, wherever they are, someday they’ll be able to ride the bus for free, eh?

https://www.cnn.com/2025/11/13/economy/job-prices-debt-economy

I know, another media anecdote. Now excuse me while I disappear for a while. Gotta prime for the game tonight.

Good grief thanks for the reminder. Would have completely forgotten the jets are playing and missed the game. Good to see you can afford an expensive prime subscription in addition to those lavish worldwide tours.

I have said the answer to your $35k income problem is providing tools to increase their skills and access to better employment. It’s called…hmmm..what’s the word again…oh yeah…capitalism! Only the first word on this page.

giving the $35k workers housing in red hook for below market construction costs, freezing the rent, funded by forcing the wealthy to sell assets, landlords to lose money , rental properties to not meet debt obligations , and risking a decline in the future tax base needed to fund these new taxes, in already the most progressive tax structure on earth, is not how this country has thrived . There are better and less risky ways to solve the low income problem.A couple of months ago, there was a lot of chitchat about the emerging popularity of socialism on here due mostly to the rising popularity of Mamdani , and close to zero commenters here defended capitalism. Perhaps you were not participating too much on AMT then. It’s no secret consumer spending has drastically changed the last 20+ years, with subscriptions and takeout meals dominating spending , and millennials and gen z known to be big participants of both. The prime defender of socialism here, aka Hal, loves anecdotes and stories. Netflix and Starbucks was my answer to that debating strategy.I’m not specifically blaming anyone for anything, and the problem of home affordability is nothing new, as home prices in the ten years before Ten was released nearly tripled in my neck of the woods when it was my turn to be turn to be intimidated by home prices. Instead of swooning, I figured out a way. Not to say it isn’t bad or much worse now, it absolutely is, but socialism treats the problem in the entirely wrong manner. There is a much better way.0 -

I don’t think people are necessarily pro socialism as they are pro putting limits and constraints on transnational capital and trying to recreate the policies that once allowed for more upward mobility. But now that those common sense policies have been repealed in the name of short term profit year after year, anyone even mentioning pumping the breaks or reigning things in gets labeled as some kind of socialist. We wouldn’t even be here if not for western capital sending jobs away, government cutting taxes for the rich, and expecting people to live in austerity in order to build wealth. The wealthy broke the system and they should have to pay more to fix it.Scio me nihil scire

There are no kings inside the gates of eden0 -

static111 said:I don’t think people are necessarily pro socialism as they are pro putting limits and constraints on transnational capital and trying to recreate the policies that once allowed for more upward mobility. But now that those common sense policies have been repealed in the name of short term profit year after year, anyone even mentioning pumping the breaks or reigning things in gets labeled as some kind of socialist. We wouldn’t even be here if not for western capital sending jobs away, government cutting taxes for the rich, and expecting people to live in austerity in order to build wealth. The wealthy broke the system and they should have to pay more to fix it.Without getting too much into details, Mamdani is targeting a select few taxpayers to fund $9 billion in new govt spending, not counting the tripling to the debt load and related service costs he wants to incur. It’s a very easy tax to avoid, which puts the city at risk of default. Although the Rs just passed a terrible tax law benefiting the rich, the USA does have one of the most progressive tax structures in the world. And literally, Mamdani has said he was a socialist and believes seizing the means of production was the end goal of his political ideology.0

Categories

- All Categories

- 149.2K Pearl Jam's Music and Activism

- 110.4K The Porch

- 290 Vitalogy

- 35.1K Given To Fly (live)

- 3.5K Words and Music...Communication

- 39.5K Flea Market

- 39.5K Lost Dogs

- 58.7K Not Pearl Jam's Music

- 10.6K Musicians and Gearheads

- 29.1K Other Music

- 17.8K Poetry, Prose, Music & Art

- 1.1K The Art Wall

- 56.8K Non-Pearl Jam Discussion

- 22.2K A Moving Train

- 31.7K All Encompassing Trip

- 2.9K Technical Stuff and Help